What is an Income Statement?

Eliza Helweg-Larsen

Published Date

An Income Statement is a history book of the sales, costs, and expenses over a given period of time. Publicly traded companies are required to publish Financial Statements (including Income Statements) as part of their quarterly and annual financial reports to provide transparency to investors, regulators, and other stakeholders about their financial performance and profitability.

Preparing the Income Statement

The top line of the Income Statement is Sales; the bottom line is the Profit (or Loss)--it is how much money you have left after all the costs and expenses of the business have been taken into account.

Income Statement Equation:

Sales Revenue – Costs & Expenses = Profit

How to Prepare an Income Statement: A Series of Subtotals

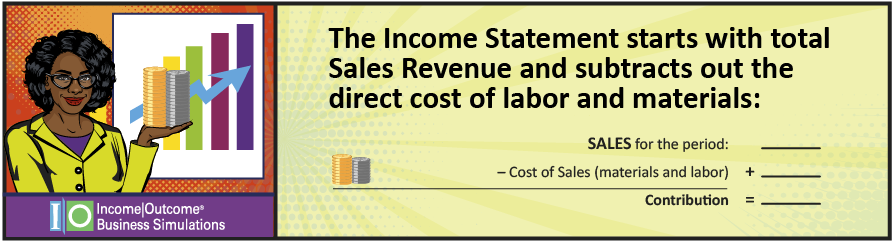

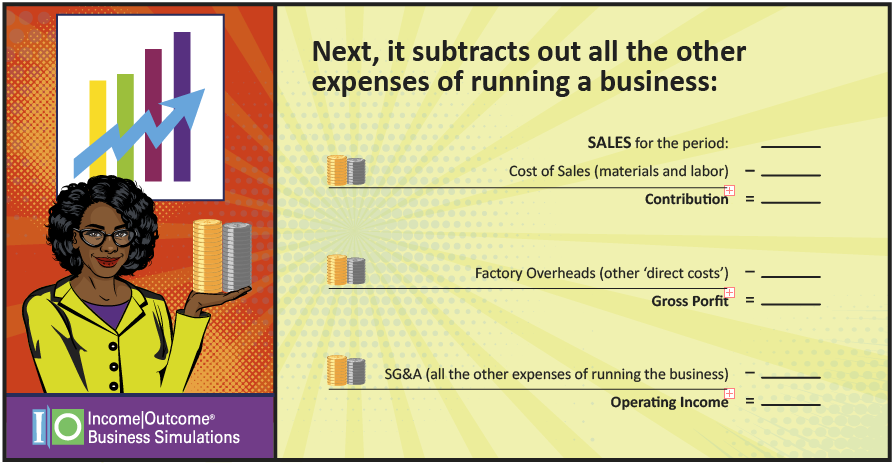

The Income Statement starts with the total Sales Revenue and subtracts out expenses until you are left with Profit (or Net Income) at the bottom line.

The first subtraction you make from that number is the Cost of Sales or COS. Cost of Sales is the direct cost for your good or service - it’s an expense that increases every time you make an additional sale. For example, if you sell another hamburger, you are using up another bun and patty.

- Direct Costs include Labor and Materials. Some companies may also include specific overhead costs such as site overheads (utilities, rent for an extra retail location), depreciation, and sales commissions

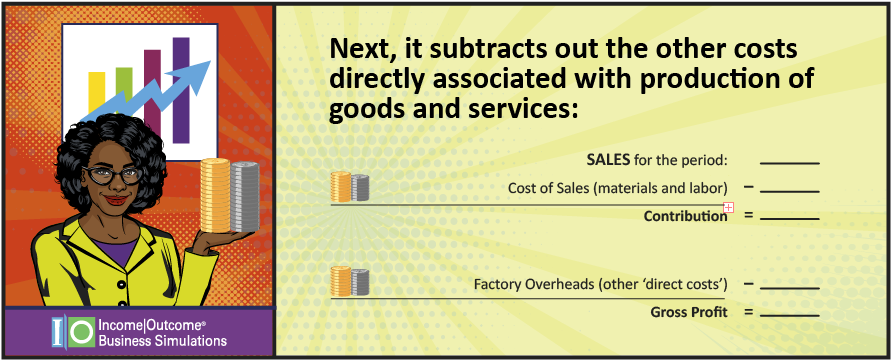

Next, you look at all the other expenses associated with the site where the activity happens. These could be factory- or restaurant-specific or more general costs such as electricity, water, and the depreciation of assets. Also, include any other site overheads at this stage.Subtract from the previous subtotal. The new number is your gross margin.

The next subtraction involves the administrative expenses and all other expenses of running a business, including R&D and salaries.When you subtract those, the next subtotal is your operating income or earnings before interest and tax. It's known by several different names, but they all mean, in effect, the operating profit for the company–the day-to-day profit, not taking into account the income tax or the cost of loans.

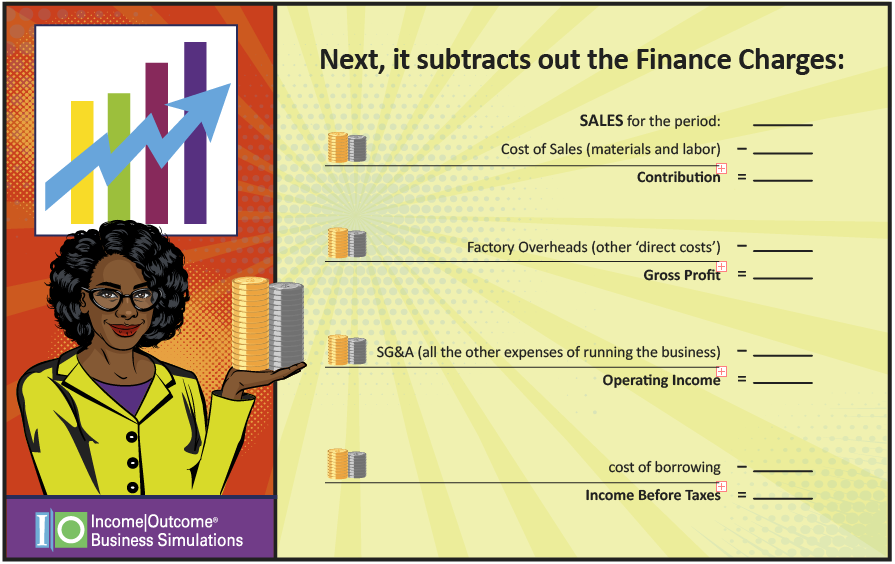

Below that, you have the finance charges associated with borrowing money, issuing bonds—or wherever you're getting the money to run the business.Subtract that number to receive your taxable income.

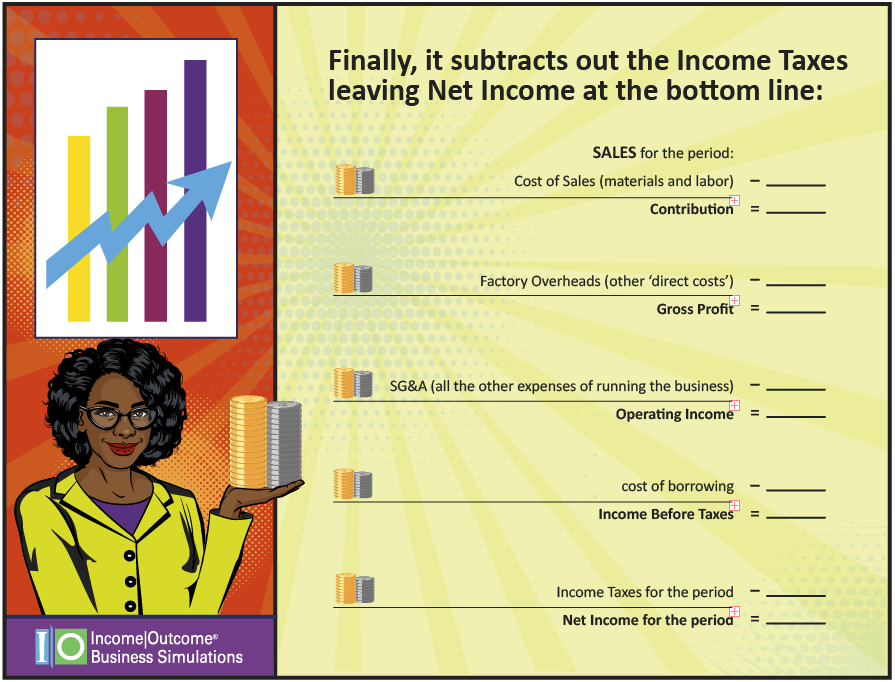

And finally, you have the taxes you pay on whatever you had left in the way of profit.Once you've subtracted the income tax, you've taken care of everything. If so, you are down to your net income, the final line and stage on the income statement.

The income statement is sometimes called a profit and loss (P&L) statement; each line on it might be called different names by various companies. But the essential structure of an income statement will always be the same. There are slight exceptions, but they are rare.There is another notable aspect of the income statement's structure. The further down the income statement you have control, the more senior you are in the company.The frontline employees only impact the sales and direct costs of the product. The managers are responsible down until the operating profit. But only the senior people in the company have any control over the finance charges and taxes. These expenses depend on where money is raised and where the business or factory operates.

A Real-World Application

Here's how this term is probably used in your office:A sales manager might suggest that salespeople look at a customer's income statement. This request aims to see if the customers are profitable or running on razor-thin margins.If they're profitable, the salespeople shouldn't need to give as much ground on the price. And if they are on razor-thin margins, the salespeople might be able to offer them a bulk discount so that they're not paying as much per unit. That is if the customer won't mind carrying an inventory for a longer period of time.

Income Statement Limitations

There is a big difference between cash and profit. You may be profitable on paper while the customer still hasn't paid yet. The income statement tells you whether you're profitable or not, but it doesn't tell you when you'll get the cash from any sales you make.It also doesn't tell you if you're making good use of your assets or if you're going to stay afloat. When you don't know when cash will come in, you don't know if you've got the cash flow to survive. Still, there's a good reason the income statement is widely used.

The Importance of the Income Statement

The income statement is one of the most important statements to reference to determine the state of a company. It is a pillar of financial reporting, along with the balance sheet and the cash flow statement. It's a thorough revenue report and is highly beneficial as an observational tool for potential investors. Visual finance is the most effective way to teach income statement information to all employees. Seeing the moving parts of the statement helps people learn far more effectively than just staring at the numbers on an income statement, regardless of their position within the company.At Income|Outcome, we offer corporate business simulation training that utilizes visual finance to teach business acumen. The simulation game board shows the connections between an income statement and a balance sheet. Participants work through the simulation, learning to analyze the income statement and balance sheet. Participants then use the information to make business decisions and achieve the best financial results for the company. Contact us if you'd like to learn more about participating in a visual finance simulation and upskilling your employees through corporate training simulations.